- Big Business This Week

- Posts

- Does the private credit crisis have echoes Of 2008?

Does the private credit crisis have echoes Of 2008?

Plus: Polymarket traders give a 69% chance of the Iran War ending by June 30

Peter S. Green

March 19, 2026

If you asked anyone in 2007 what a “subprime mortgage” was, they wouldn’t have any idea. So here’s a question for you: Do you know what the private credit market is?

Here’s why your answer matters: When prominent U.S. financiers start drawing parallels to the Great Recession of 2008, it might be time to worry. And yes, this time around, yet another little-known investment vehicle has people increasingly concerned.

At its simplest, private credit is a loan made to a company by a non-bank lender. In the traditional world, if a business needed money to grow, it went to a big bank (like Chase $JPM ( ▲ 0.27% ) or Wells Fargo $WFC ( ▲ 1.19% ) or issued bonds on the public stock market. In private credit, that middleman bank is removed. Instead, the business borrows money directly from a private investment firm.

The advantage for borrowers is that they can get cash quickly in a squeeze, and they don't need to show the same financial solidity as they’d need for a loan from a bank. When times are good, investors like the higher interest rate and the supposedly guaranteed return that private credit loans offer. But now a confluence of forces is raising questions about how strong the private credit market really is. The scale of a possible looming crisis could bring down confidence in the broader stock market.

Doubts about private credit have already spread so far that some of the major publicly traded firms making a lot of private credit loans have seen a sudden and significant drop in their share prices this year, including giants like Apollo Capital Management $APO ( ▲ 4.44% ) (down 25% this year), Ares $ARES ( ▲ 3.2% ) (down 36% this year), Blackstone $BX ( ▼ 0.25% ) (down 30% this year) and Blue Owl Capital $OWL ( ▲ 1.38% ) (down 41.5% this year).

What’s the problem? In a word, the private credit giants got overextended. They began offering private credit exposure to retail investors through the big brokerages (known in the investing world as “wire houses”), just as interest rates are failing to come down, and the war in Iran is making small investors nervous. Now, too many investors want to cash out, or redeem their investments. The tide is going out, and the question is: Which borrowers were swimming naked?

Speaking of the borrowers: A large amount of private credit has been extended to tech companies, many of which have suddenly seen their business models turned upside down by AI, especially those Software-as-a-Service companies whose proprietary cloud software is easily cloned or replicated by Claude and his posse of profit-killers.

The biggest difference between private credit and traditional means of business financing, like bank loans, stock offerings, or bond issuing, is the absence of organized exchanges to trade and price the loans, and a lack of information about the vast bulk of private credit loans.

That murkiness increases not just the perception of risk, but real risk, and it means that when investors get spooked, it doesn’t take much to start a run. That’s what happened last month, when Blue Owl Capital saw its investors trying to cash out. They were asking for more cash than the borrowers were paying on their loans each month. So Blue Owl capped so-called redemptions, but that just sent its share price tanking. That’s when former Pimco CIO Mohamed El-Arian,a well-regarded financial prophet, asked if private credit marks are seeing their “canary-in-the-coalmine moment,” much like the 2007 beginnings of the mortgage crisis that provoked the Great Recession. Here’s his Tweet:

There are indeed some strong parallels between 2008 and 2026: For one, no one is quite sure how large the private credit market is. Estimates range from about $1.7 to $2 trillion, a relatively small chunk of the $40 trillion U.S. commercial debt and credit market. But many investors don't know just how much risk they are actually carrying. Borrowers don’t have to provide the same level of financial information they do to the stock market, and that private credit debt can get sliced and diced into tranches of varying creditworthiness, the same way mortgage-backed securities were, back in the aughts.

Then there’s the contagion factor, which works two ways. The first is contagious fear: As more investors try to redeem, the headlines get worse and still more investors want to find a safer haven. The other contagion factor: When private credit borrowers default, they’re taken over by the private credit lenders. That means no cash flow from interest payments for the syndicates, but it also means equity investors — and these firms tend to have large private equity investors waiting for an IPO payday — are hit with a huge loss. That contagion can reverberate around the financial system, much as the commercial and subprime mortgage defaults hit an over-leveraged financial system in 2008.

So how bad is it? For now, cool heads seem to be prevailing. Kaush Amin, head of private market investment at U.S. Bank, says the fears are overblown. “The numbers are still not showing broad-based stress,” Amin said in an interview. And while some private credit borrowers, especially those whose business has been upset by AI, tariffs or interest rates (think commercial real estate) may end up forcing lenders to write down their loans, there’s less sense of a systemic threat, for now, to the financial system, the way there was in 2007 and 2008. “A lot of these are cash-flowing companies, so I don't think they'll have an issue servicing the loan. The biggest issue right now that we see is that sentiment is driving redemption requests,” said Amin.

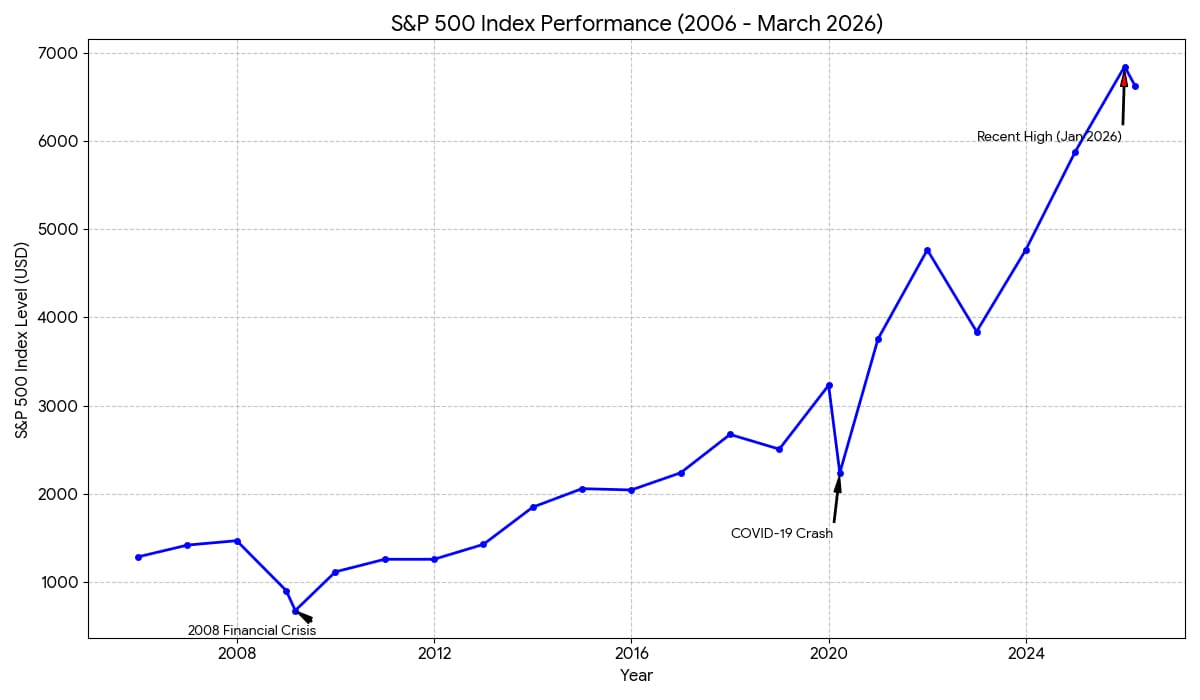

It’s also worth remembering that for retail investors who kept their money in the market during 2008, the subsequent rewards have been substantial:

Stock market performance from 2006 to 2026. That tiny blip in the bottom left-hand corner is the 2008 financial crisis. Image credit: Google’s Nano Banana Pro, based on $SPX ( ▲ 0.7% ) S&P500 data.

Still, at least you know what the private credit market is, now. Let’s hope you won’t be hearing much more about it over the coming months.

Big Businesses mentioned this week:

$APO ( ▲ 4.44% ) $ARES ( ▲ 3.2% ) $BX ( ▼ 0.25% ) $OWL ( ▲ 1.38% ) $WBD ( ▲ 3.26% ) $PSKY ( ▲ 1.92% ) $NFLX ( ▼ 2.0% ) $AAL ( ▼ 1.04% ) $UAL ( ▼ 1.81% ) $DAL ( ▼ 1.3% ) $LUV ( ▼ 1.38% ) $IAG ( ▼ 2.54% ) $LHAI ( ▲ 5.65% ) $QAN ( 0.0% ) $MSFT ( ▲ 3.02% ) $GOOG ( ▲ 6.88% ) $CME ( ▲ 0.21% ) $NYT ( ▼ 1.24% ) $TSLA ( ▲ 0.76% )

This week, big business!

The war story

Flash, bang, boom! Oil and gas prices are shooting up, as the War on Iran rolls on without a clear end plan. A direct Iranian strike overnight Wednesday on the world’s largest liquified natural gas facility at Ras Laffan sent oil prices up to $119 a barrel for Brent crude May delivery, before dropping to $114, a 7% overnight climb, and up nearly 80% this year. The front-month gas price in the Netherlands, a European benchmark, jumped 16% to 63.42 euros a megawatt-hour. U.S. natural gas prices jumped 2.8%, and U.S. gasoline futures hit $3.18 a gallon for April delivery, up 2.6% overnight to a high last seen at the end of the pandemic. None of this is good news for the world economy. Oil prices are likely to keep rising into the high-$100+ a barrel range, says Rapidan Group’s Bob McNally, a leading energy strategist, before plummeting as the world enters a recession. "They grind higher until they cause pain, enough pain to slow the economy and demand dissipates, and we get a free fall," McNally told Business Insider. The problem is that oil won’t peak until either Iran’s ability to block the Strait of Hormuz is wiped out, or Israel and the U.S. negotiate an end to the fighting. But analysts say the killing of top Iranian leaders may have left the country without a central command and control structure, leaving no one to negotiate with and leaving individual military units to choose their own targets. Bettors on Polymarket give a 69% chance of the War ending by June 30:

Image source: Polymarket odds on the end date of the Iran conflict.

Jonesing for a ship: In a desperate effort to help keep the price of oil and food from climbing even further, President Trump has waived the Jones Act, a 1920 federal law that says only U.S.-made and crewed ships can carry cargo between U.S. ports. The waiver is unlikely to do much to bring down consumer costs. While gasoline is up about 30% per gallon(about 85 cents) since the war started, an MIT study found that the Jones Act added only about 1.5 cents a gallon to the price of gasoline. The U.S. shipping lobby is incensed: “We will be watching closely,” warned the American Maritime Partnership. The group says the bill protects American jobs.

Friendly Ghost Fleet? The Trump Administration has lifted restrictions on Iranian-owned tankers that are part of the sanctions-busting ghost fleet that’s been bringing Iranian oil to China and other countries. Trump also lifted sanctions on Russia’s ghost fleet, letting the Putin regime sell as much as $1.2 billion a day in more oil to support its war in Ukraine. Just last month, the U.S. slapped new sanctions on 14 Iranian tankers that the State Dept. said were funneling money to Tehran used to “support terrorism abroad and repress its citizens.” Oil prices spiked after Iran said it laid mines across the 21-mile-wide Strait of Hormuz, through which nearly all Arab and Iranian oil, about 20% of the world’s supply, has to pass. But according to Lloyd’s List Intelligence, some 90 ships have passed through the strait since the U.S. attacked Iran on Feb. 28. Trump is betting that keeping the oil flowing could help bring down prices, which have shot up more than 40% since the war started.

Meanwhile, holding on to tankers seized from Venezuela is getting expensive for the Trump Administration. One seized tanker, Skipper No. 9304667, has cost the U.S. $47 million over the past three months in maintenance, repairs, insurance, crew wages, and storage fees for the ship’s oil. The ship is only said to be worth about $10 million, and its oil cargo worth about $120 to $135 million at current prices.

ADVERTISEMENT

Attio is the AI CRM for modern teams.

Connect your email and calendar and Attio instantly builds your CRM. Every contact, every company, every conversation — organized in one place. Then ask it anything. No more digging, no more data entry. Just answers.

END OF ADVERTISEMENT

The usual suspects

Cashing out: Departing Warner Bros. Discovery $WBD ( ▲ 3.26% ) CEO David Zaslav may have killed off one of Hollywood’s most storied studios, but he’s laughing all the way to the bank. Zaslav is set to exit with more than $800 million in severance and other payments, according to an SEC filing, including a tax payment worth about $130 million, if the planned sale to Larry and David Ellison’s Paramount Skydance $PSKY ( ▲ 1.92% ) goes through. Had Netflix $NFLX ( ▼ 2.0% ) won the bidding for WBD, the tax payment wouldn’t have been needed. WBD’s share price is down about 25% since it was first announced that Zaslav would be leading a merger of Warner Brothers with Discovery, back in 2021.

Fly-By: Iranian rockets and sky-high fuel prices aren’t keeping Americans from taking to the air, even as ticket prices rise an average of 10% to cover the higher costs, airline execs said at an industry conference this week. American $AAL ( ▼ 1.04% ) , United $UAL ( ▼ 1.81% ) , and Delta $DAL ( ▼ 1.3% ) each said they expect to pay an extra $400 million for fuel this year, but were leaving their profit forecasts unchanged. The U.S. Global JETS ETF, a good proxy for airline stocks, is down more than 18% in the past month. You know what else is down? Southwest’s $LUV ( ▼ 1.38% ) tolerance for hefty passengers. Once known for accommodating large travelers, Southwest is now getting flak from fat flyers for forbidding them from flying unless they purchase an extra seat. The National Association to Advance Fat Acceptance says Southwest has become “much more aggressive” at identifying tubby travelers. Southwest has been struggling over the past year or so. The war has been a disaster for the three giant Gulf-based airlines, Emirates, Qatar Airways and Etihad Airways. They’ve turned the Gulf into a hub that handled 227 million passengers last year, and with more than 50,000 flights cancelled since Feb. 28, the total cost to the airlines plus tourism in the Gulf could hit $56 billion this year, according to an analysis cited by the New York Times, and it’s hurting places like India and Southeast Asia that rely on visitors who transit through the Gulf. That could be a bright spot for competitors based elsewhere. British Airways and Germany’s Lufthansa $LHA.DE are adding seats to long-haul flights that bypass the Gulf, as is Australia’s Qantas $QAN.AX.

The Pentagon is doubling down on its “anti-Woke” attack on Anthropic, which is so far the only AI to pass the Defense Department’s security screenings. In federal court filings, the Pentagon said itquestioned whether Antropic was a “trusted partner” and would introduce “unacceptable risk” into military supply chains. That followed a threat last month by Defense Secretary Pete Hegseth, to declare Anthropic a “supply chain risk,” after the firm said it didn’t want Anthroppic’s AI used for mass domestic surveillance or to develop and run autonomous killingmachines. Microsoft $MSFT ( ▲ 3.02% ) filed a brief supporting Anthropic, as did a group of 37 OpenAI and Google $GOOG ( ▲ 6.88% ) engineers.

Taking Banksy to the Bank: The elusive British graffiti artist has finally been tagged: He’s a 50-ish man named Robin Ginnigham, from Bristol on the west coast of England. What’s in a name, you ask? Money, it turns out. Collectors, who have paid as much as $24 million for Banksy’s work say knowing the artist’s identity ultimately means it’s easier to be certain a work is genuine, keeping prices high.

Image credit: Banksy Google’s Nano Banana Pro

Trumplandia

It ain’t happening: That’s a rate cut for 2026. Rising inflation from the Iran War oil crisis speaks louder than anything President Trump can say: The Fed’s Open Market Committee said Wednesday it won’t be cutting rates any time soon, avoiding talk of the war, with Fed chair Jerome Powell saying the economy and labor markets are in good shape, and core inflation (not including energy) is likely to moderate in the coming months. That means no need for a rate cut. What went unsaid was the war. “Investors concluded that monetary policy may be limited in its ability to address the war’s economic consequences,” investor Fred Yardeni wrote in a note posted after the Fed meeting. Powell’s intended successor, the yet-to-be-confirmed Kevin Warsh, has been under pressure from President Trump to lower rates to help shrink the national debt and boost the economy, but that’s probably on hold for now, and futures markets now put the odds of a 0.25% cut in benchmark rate at just 17.2%.

No more quarterly earnings releases? The SEC is preparing a proposal to let publicly traded companies report their earnings only twice a year, instead of every three months, as they’ve been required to do for more than half a century. The idea is supposedly to reduce the burden on public companies, but investors fear a lack of transparency would affect the security of their stock holdings. Europe and the UK have botched relaxed quarterly reporting requirements. The proposal has yet to be made public, and it will be open to hearings, and then the SEC itself will vote on whether to enact the rule.

The family business: Even as Jared Kushner jets around the Middle East trying to broker a peace deal alongside his father-in-law’s special diplomatic envoy Steve Witkoff, Kushner is also soliciting Middle East government to invest some $5 billion in his investment firm, Affinity Partners, The New York Times reports, citing people with knowledge of the solicitations. Among Kushner’s targets: Saudi Arabia’s Public Investment Fund. Kushner said in 2024 that he wouldn’t blur public and private lines by seeking investments while Trump is in office. But new fundraising documents say that Affinity has already invested close to $4 billion of the $5 billion it’s raised, and claims a 25% annual return.

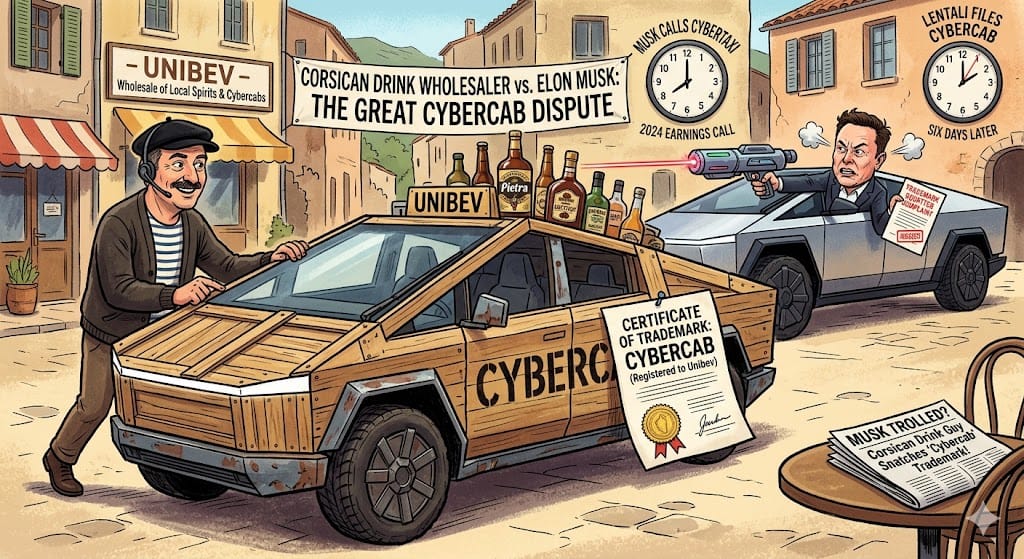

Trolling Elon? A Corsican drink wholesaler called Unibev says it owns the trademark “Cybercab,” setting up a major trademark dispute that could dog Tesla $TSLA ( ▲ 0.76% ) as it prepares to manufacture driverless taxis under that name. Tesla notes that the French company has never built a car of any kind, and its CEO, Jean-Louis Lentali, is a regular on Tesla’s quarterly earnings calls. The Musk-led car maker has filed a complaint with the U.S. Patent and Trademark Office, calling Unibev a “trademark squatter.” Lentali filed a trademark application six days after Musk first used the word Cybertaxi on a 2024 earnings call. It took Tesla six months to file its own trademark application for the name.

Image credit: Google’s Nano Banana Pro

Want more Cheddar?

You’re clearly into smart people talking about even smarter things. Lucky for you, that's literally our whole deal at Cheddar. We interview the brightest minds in business, finance, and tech. If you'd like more in-depth analysis from interesting people, lcheck out our where to watch page and turn us on 24/7! Your wallet will thank you and so, more importantly, will your mind. But also your wallet. Remember that.

Peter S. Green is a veteran reporter and editor who has spent more than two decades covering business and finance from Eastern Europe to New York City, and has worked for Bloomberg News, The New York Post, The New York Times and The Messenger. He lives in New York City and is always looking for the next big story. Email him here.